The Hidden Reasons Why You Can’t Afford A House

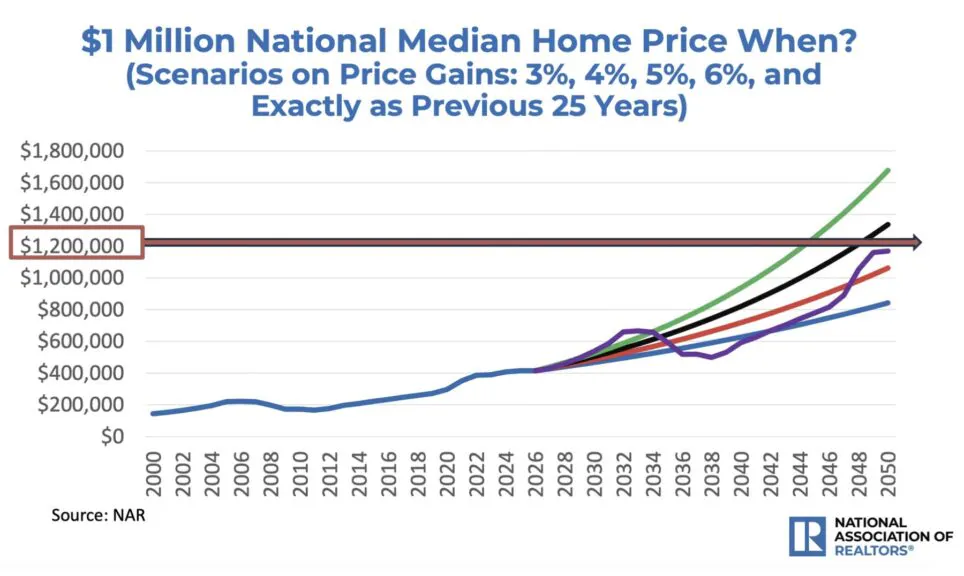

Here’s a headline you probably haven’t seen, even though it will have more impact on your life (and your children’s lives) than anything coming out of the Middle East: By the time millennials hit retirement age, the typical home in this country will cost $1 million. That will be the median price of a home — not just new homes, but any home — by 2050.

Live Your Best Retirement

Fun • Funds • Fitness • Freedom

Put another way, if you have a child today, by the time your child is looking for a place to live, they’d better have $200,000 saved up for a down payment. And for the rest of their lives, in all likelihood, they’ll be paying off a debt that’s completely insurmountable.

This isn’t a projection from some crackpot looking for attention. It’s coming from one of the top housing economists in the nation:

“Essentially, in about 25 years the national median home price will be a million dollars,” Lawrence Yun, chief economist at the National Association of Realtors, said at a conference in Washington, DC, on Tuesday. “It may be hard to envision that, but back in 1990, the national median price was $90,000.” Yun noted that even San Francisco, considered an exorbitantly priced real estate market at the time, had a median price of only $250,000 in 1990.

For comparison, as of right now, the national median sales price for existing homes is roughly $430,000. So as high as housing prices are right now, you can expect them to be much higher — more than double — in just a couple of decades.

This economist “used multiple scenarios to project home prices out into the future, and says each scenario pointed to roughly the same timeline to hit $1 million: about 25 years.”

To be clear, although the economist determined that we’d hit $1 million as part of ordinary appreciation in home prices, inflation isn’t the only factor here. Inflation alone won’t get us to this figure. And there’s reason to believe that typical home prices will actually exceed $1 million by 2050, by a lot.

But first, I want to discuss the story of 31-year-old Micah Longmire. This is a true story. I found the details in a small online-only paper called The Missoula Current.

According to the paper, Micah earns a salary of $200,000 a year. That’s a high salary by any measure — more than double the median household income in this country. The average lawyer in this country doesn’t make $200,000. So you might think Micah is doing pretty well, all things considered.

But after looking all over the country for more than two years, Micah and his wife determined that they couldn’t afford to buy a home on their own — at least not without taking on a mortgage they weren’t sure they could afford.

Yes, even though his salary puts him in the top 10% of American incomes, he wasn’t able to lock down a home despite looking for two years in a variety of markets.

In the end, Micah’s solution was to pool some money together with his wife’s parents and, together, they bought a 3,500-square-foot, $600,000 home in Chattanooga, Tennessee, for the entire family.

Micah now lives with the in-laws. And as he put it, “I make $200,000 and I wouldn’t have been able to buy a house by myself. That’s ridiculous.”

Now you can take issue with the idea that Micah truly couldn’t afford a home. Many of you probably purchased a home with an income lower than $200,000. And you might think that he could’ve picked a smaller house, in a different area, and everything would’ve been fine.

But before I address that objection, I need to make the point that Micah’s story is not unusual. Just a couple of days ago, Fitch — one of the big three global credit rating agencies — downgraded the U.S. homebuilding sector from “neutral” to “deteriorating” because people aren’t buying homes anymore.

30-year mortgage rates are over 6%. Consumer sentiment — meaning, how pessimistic people are about their finances — is at a record low. Going back to the 1950s — even through the 2008 financial crisis — the surveys of consumer sentiment weren’t as dire as they are right now.

So while it may be the case that people like Micah could theoretically purchase a home if they were willing to make more compromises, the fact remains that they aren’t doing that. And we need to figure out why.

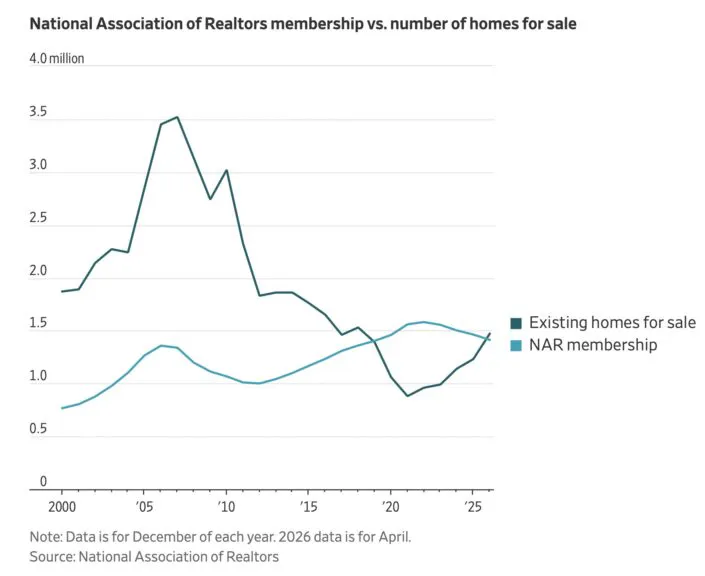

I’m not cherry-picking anecdotes or statistics here. Every possible indicator is sending the same signal. Here’s another one: Real-estate agents are quitting in droves.

This is data from the National Association of Realtors. It shows the number of members in the realtors’ association (light blue) and the number of existing homes for sale (darker line).

From 2012 to 2022, membership in the association grew every single year. Now it’s declining steadily. The association of realtors now has just 1.4 million members, compared to 1.6 million in October 2022. And as the chart shows, for most of this century, there have been far more homes for sale than realtors. The ratio was healthy.

But that hasn’t been the case for several years now. Realtors are competing over a very small number of homes. And on top of that, a recent legal settlement means that realtors have to disclose their fee upfront, which is leading many home buyers to handle the process themselves.

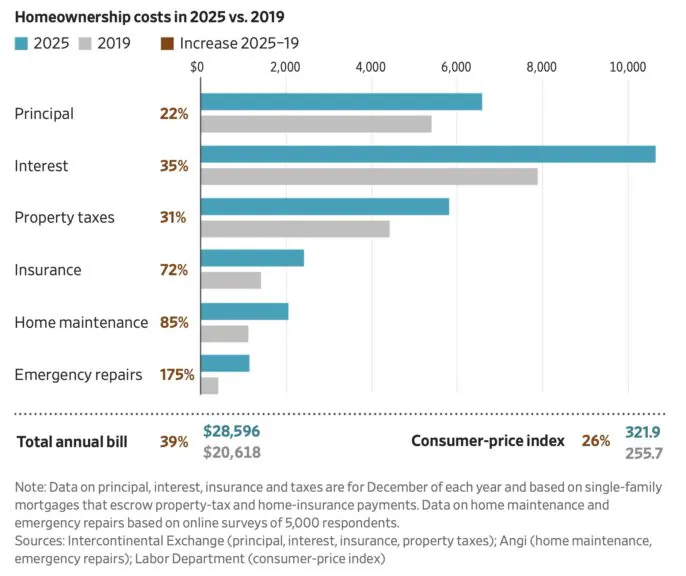

To give you an idea of how quickly the housing market has become unaffordable, take a look at this chart from the Wall Street Journal the other day. They’re getting their data from the Intercontinental Exchange, Angi, and the Labor Department.

If you’re buying a home now, as opposed to 2019, then on average you’re paying 22% more in principal, 35% more in interest, 31% more in property tax, 72% more in insurance, 85% more in home maintenance, and 175% more in emergency repairs. Your total annual bill is 40% higher than it would’ve been just six years ago. If you’re the average American, your annual expenditure on housing went from $20,600 to $28,500.

The Journal reported:

Sales of previously owned homes have held around 4 million a year since 2023, the lowest level in decades and down from a pre-pandemic norm of between 5 million and 5.5 million a year, according to the National Association of Realtors. That means fewer prospective buyers are accessing homeownership. … And many of those who are buying homes are stretching their budgets to do so. Those new homeowners are vulnerable to falling behind on payments if their incomes drop or they face unexpected jumps in homeownership costs. .. A buyer with a $2,500 monthly budget and a 20% down payment can afford to buy a $517,500 home at a 3% mortgage rate, according to real-estate brokerage Redfin. At today’s rate around 6.5%, that same buyer can only afford a $384,000 home. Even though rates have climbed, typical home values remain near record highs, according to Zillow, confusing many buyers who have been waiting for prices to fall.

That last part is important. Normally, when interest rates go up, you expect home values to go down. You’re paying more for interest over time, so you expect that your upfront costs will be lower. This is normally how things work, and it makes a lot of sense.

But in practice, it’s just not happening anymore. In most markets, there’s nothing to offset the high interest rates. The homes have higher list prices and higher costs over time. It’s a lose-lose.

One of the reasons that the conventional wisdom doesn’t apply anymore is that no one wants to sell their home. And why would they? In many cases, they locked in an extremely low interest rate during the pandemic. And as we’ve already discussed, they can expect a very large return on their investment in the coming decades. But even after several decades, they won’t want to sell, because their children will need somewhere to live. If the median home is going for $1 million, then many more homes are going to remain in the family.

But what if I told you this is an incomplete picture of what’s going on? And in fact, there was plenty of affordable housing in America. Here’s an experiment: take a look at this $700,000 home in San Francisco, California, one of the most desirable and expensive housing markets in the country. It underscores just how bad things are out there:

It’s a 1200-square-foot dump. The listing calls it a “diamond in the rough” with “immense potential,” which is always a good sign. When you’re spending $700,000 on a home, that’s exactly what you want — “immense potential.” We’ve all come to accept this kind of price disparity because of the principle of supply and demand. So we don’t think about it.

But here’s what you can get for the same price in Detroit, Michigan — a far less desirable or expensive housing market than San Francisco.

$700,000 in the Midwest gets you basically a castle: It’s 5,300 square feet, with five bedrooms and a wood-paneled library. It’s centrally located. Fifteen minutes to downtown. Twenty minutes to the airport.

A home that would be at least $2 million in Nashville, New York, or Los Angeles, or even in suburban Detroit. Now $700,000 certainly isn’t cheap, but that’s not the point. The reality is that real estate markets are hyper-local, and there are pockets of affordability out there. You can still buy nice, livable $250,000 homes in many rural areas or small cities like Toledo, Ohio.

So what’s really going on with housing?

This is the first big issue with housing: everyone wants to live in the same places, which is driving prices in those places up astronomically.

San Francisco, New York, Boston, and Nashville are boom towns. Detroit, Fort Wayne, and Gary aren’t. Though — to be fair — this is starting to change, and the Midwest is posting its first net-migration gains in decades, driven largely by relative affordability compared to the coasts.

One factor driving this is jobs. San Francisco is the tech capital of the world. They have a lot more jobs out there. But that’s still kicking the can down the road. It’s not addressing the fundamental issue, which is that something caused cities like Detroit to become undesirable investment opportunities for job creators.

Yes, the auto industry took a major hit. That’s the default explanation for what’s happened here. But plenty of industries in San Francisco have died since the 1960s as well. San Francisco used to be a manufacturing powerhouse. There was a major shipbuilding presence in the city. They also refined a lot of chemicals. Not anymore. It’s moved across the Bay. So in many historical respects, San Francisco and Detroit are more similar than they appear. But over the past half-century, one city managed to attract job seekers and investment, while the other died out.

This brings us to the second reason housing is out of control. Urban crime has made many cities unlivable, which has led millions of people to rule out some of the prime real estate in the country.

If you look at the demographics, the distinction between the two cities is hard to miss. San Francisco is around 5% black. Detroit is closer to 80% black. And as you’d expect, based on the statistics, Detroit has three times the violent crime rate of San Francisco.

Could that be why no one wants to live there? In school, you’re taught that the causation works the other way — that these cities are violent because they’ve been abandoned and forsaken by everyone else. But maybe it’s the opposite — maybe these cities have been abandoned and forsaken precisely because they’re violent and dysfunctional. And maybe, if we address the violence and the dysfunction, then virtually overnight we can have infinitely more housing stock than we do right now.

You never hear about cleaning up the streets — going full “Citizen Vigilante” on criminals — expressed as a housing policy. But that’s exactly what it is. It’s the single most straightforward way to address a problem that we all know exists.

Detroit’s an interesting case study on this. Since the city’s bankruptcy in 2013, a consortium of billionaires has revitalized the downtown, which is now a thriving commercial district. They did this in conjunction with the city and state, which started aggressively policing the area, and by encouraging downtown businesses to hire private security.

As the downtown and surrounding areas became safer, people started moving back into the city. If those trends continue, hundreds of thousands of vacant homes in Detroit could come back online.

But despite those successes, no one is supposed to even float the idea of fixing the cities. Instead, the universal message is that we just have to accept the way they are.

Ed Sheeran went on Theo Von’s podcast to talk about how London is “sketchy” and dangerous now. And instead of suggesting that the government fix the problem, he says the solution is to make sure you’re not carrying anything that criminals might want to steal.

Watch:

Ed Sheeran: Every single area of London is sketchy.

Nice neighborhoods, bad ones, doesn’t matter. Just don’t walk around with a Louis Vuitton bag and a £200k watch.

Theo Von: “But y’all’s robberies always have clues though.”

Ed: “I love that you think of England like it’s a… pic.twitter.com/fvHgkzzyTV

— Camus (@newstart_2024) June 21, 2026

That’s got to be one of the most relatable pieces of advice ever dispensed by a celebrity. “If you wander around with a Louis Vuitton and a $200,000 watch, you are going to get robbed. Just don’t do that.”

Of course, when he’s spending time in his $27 million mansion in London, or driving through the city in an armored SUV, or walking around with armed bodyguards, Ed Sheeran probably isn’t taking his own advice. He has no reason to.

But for everyone else — for people who can’t spend millions of dollars on a home — the message is that you’re responsible if you get robbed, assaulted, and murdered. It’s not the fault of the criminals. They didn’t do anything wrong. You’re the one who should suffer because you made yourself a target by existing.

You have two options: Get robbed and shot, or do what everyone else is doing, and move far away to a coastal enclave, or a pocket of the South or the Mountain West. And naturally, if you do what everyone else is doing, you’re going to pay a lot more.

That some of the most desirable areas of the country have been made undesirable because of post-Civil Rights Movement realities — is compounding the first issue — that millions of people want to live in the same small number of places.

But there’s a third factor in all of this, which is commonly overlooked: illegal immigration driving demand for new homes.

If it’s true that 20 million illegal immigrants or more arrived here during the Biden administration, then they had to live somewhere. And in fact, James Carter, a former deputy assistant Treasury secretary, wrote an op-ed a couple of days ago in which he spelled out the extent to which illegal aliens have caused housing prices to increase so much over the past few years:

For much of the 2010s, pay in lower-skill occupations lagged behind while professional salaries pulled away. As immigration enforcement has increased, that gap has narrowed. Take construction, which relies heavily on immigrant labor. Wages in the sector grew at roughly 2.5% annually between 2010 and 2017. Now BLS data shows construction wages growing at 3.1% through the first quarter of 2026—above the sector’s pre-enforcement baseline, even as broader private-sector wage growth cooled to 3.4%. … A recent Federal Reserve working paper finds that unauthorized immigration accounted for roughly 30% of house-price growth and 20% of rent growth in the average metro area between 2021 and 2024.

I’ll say that last part again: Illegal aliens caused 30% of the increase in housing prices that we’ve seen in recent years. So at the same time that illegal aliens were competing for American jobs, they were causing a massive spike in housing costs across the board. I had to double-check the statistic because, even with the knowledge that Joe Biden’s administration imported tens of millions of illegal aliens, it still seems very high.

And indeed, this is from a recent paper published by the Federal Reserve Bank of Dallas:

We find that during the boom period an increase in unauthorized immigrant worker flows equal to 1% of a local area’s initial employment increased local house prices by 2.2% and increased local rents by 1.4%. The impact on rents is slightly smaller for single-family units and slightly larger for multi-family units. …. A back-of-the-envelope calculation suggests that unauthorized immigrant worker flows can explain about 30% of the total growth in house prices and 20% of total growth in rents over the boom period for the average local market.

This is one of the main reasons it’s getting harder and harder to live in a country that resembles the one Gen X or millennials grew up in. The degree to which foreigners have reshaped this country and all of the West is truly staggering to comprehend.

Take a moment now to look at all 3 factors leading to the rise in housing costs that we’ve addressed: First, that people only want to live in a few places. Second, urban crime makes many prime locations unlivable. Third, immigration has the dual issue of causing more pressure on our strapped housing market while also reducing the number of desirable areas to live. What you have between these three factors is a perfect storm. But they’re not all.

A fourth reason for skyrocketing housing costs is terrible public policy. Government regulations and codes are making it more expensive to build new housing supply, particularly in places like coastal California.

Places that have developed huge amounts of housing in the past decade — like Austin, Texas — have seen rents stabilize or even decline. Anti-growth places like Boston and San Francisco, where it’s basically impossible to build anything, have seen prices skyrocket. The U.S. population in 1990 was about 250 million people. Today it’s about 350 million people, a 40% increase.

In 1990, San Francisco had 328,000 housing units. Today, it has only 415,000, a 25% increase. The rise of NIMBYs in places like San Francisco and the counties around it is making it impossible to deal with the demand surge from a constantly growing population.

At this point, you’re probably thinking — what about places where you can build, places where there isn’t urban crime, and places without a lot of immigration? Why are places like Northern Michigan or Stowe, Vermont, or coastal Maine also getting so expensive?

Well, this is related to the previous points: people want to live in places that resemble 1950s America. Go to Vermont, coastal Maine, or Northern Michigan, and you can find that. And there’s a huge trend of people fleeing diversity to those areas.

But there’s also a very important and overlooked fifth reason for rising homeownership costs: inflation.

The government has doubled the amount of money in circulation during COVID, meaning the value of the dollar is declining, which in turn inflates the dollar cost of homes. This is one of the consequences of being $40 trillion in debt — our leaders will seek to inflate away the currency as a roundabout way of reducing the country’s financial obligations.

Inflation is a hidden tax that’s behind so many of the aforementioned price increases: a dollar in decline means home prices rising, even if the inherent value isn’t rising with it. It makes repair and replacement costs higher, which drives higher insurance costs.

It also makes it more expensive to provide city services, which means your taxes need to go up. A lot of the rise in housing prices is really just a decline in the dollar. Which is why it’s a bigger and bigger issue that young people can’t afford homes: one of the best defenses against inflation is long-term debt backed up by an asset that rises with inflation.

These five explanations for rising housing costs go a long way in explaining why we’re in the situation we’re in. And unless they change, predictions that the average house will be $1,000,000 by 2050 are likely to underestimate the situation.

The problem is that solving these problems isn’t politically practical. And for that, we can thank the most selfish generation in American history: the Baby Boomers.

Boomers today control over 40% of the national real estate wealth, and about a quarter of them own a second home or vacation property. One Northwestern Mutual survey found that fewer than a quarter plan to leave an inheritance to future generations.

A Charles Schwab survey of high-net-worth Americans found that, for nearly half of Baby Boomers, their priority is to “enjoy my money for myself while I’m still alive.” It’s impossible to overstate just how historically bizarre and evil this attitude is.

For all of human history, the thing that animated the older generations was a desire to pass down a legacy to their children and grandchildren. This is still the norm outside of the Boomers.

That same survey found that wealthy millennials were less likely to list “enjoying my money for myself” as their priority. They had a greater desire to see their own kids inherit their wealth. So the Boomers are, in this way, an aberration. Their total lack of interest in passing wealth and legacy to their children is unique, creating unique problems that their children and grandchildren have to deal with.

It’s not useful or helpful to sit around stewing in resentment against other generations. But the fact is that, economically, the Boomers did have it considerably easier than their children have it. When they started entering the housing market in the late 1960s, the dollar was still pegged to the gold standard.

The immigration laws that transformed the country had only just passed. The cities were mostly still livable (but in steep, swift decline — because of laws supported by Boomers), and it was easy to build new housing in suburbs, which were hardly regulated. Boomer NIMBYs hadn’t made it impossible to build in coastal California. Owning a home was the American dream, and it was an attainable one.

Now that they’ve secured their dominant position in the American real estate market, Boomers have done everything possible to make sure housing stays unaffordable. Doing anything that might reduce the value of their housing is politically untenable, something President Donald Trump has said out loud.

Watch:

President Donald Trump said during a Cabinet meeting on Thursday that he wants to “drive housing prices up.”

“Existing housing, people who own their homes, we’re going to keep them wealthy. We’re going to keep those prices up,” Trump said.

Trump made his comments following… pic.twitter.com/KBe8wo7Myq

— PBS News (@NewsHour) January 29, 2026

So if you’re a young person who wants a home, just know that there’s a reason it’s so bad out there: it’s because the number of desirable places is rapidly declining, lots of prime real estate is taken up by the worst and most violent people in the country, the government is deliberately destroying the value of the dollar while also importing millions of people and making it impossible to build anything new.

Now, as a result, the choice is binary and unavoidable: We can either doom future generations to a market that consists entirely of one-million-dollar homes, or we can make the decision — as unthinkable as it may be to someone like Ed Sheeran — to become a lot less tolerant.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

I am just an average American. My teen years were in the late 70s and I participated in all that that decade offered. Started working young, too young. Then I joined the Army before I graduated High School. I spent 25 years in, mostly in Infantry units. Since then I've worked in information technology positions all at small family owned companies. At this rate I'll never be a tech millionaire. When I was young I rode horses as much as I could. I do believe I should have been a cowboy. I'm getting in the saddle again by taking riding lessons and see where it goes.

Comments (0)